How to Build Custom Fraud Prevention Rules

Design, test, and deploy custom fraud prevention rules—combine signals, reduce false positives, and monitor performance to protect revenue.

Fraud prevention rules are automated tools that help detect and block fraudulent activity by analyzing transaction details like amounts, IP addresses, and behavior patterns. These rules follow a clear structure: {action} if {condition}, allowing businesses to block, review, or verify transactions based on specific criteria. For example, you could block transactions over $1,000 for first-time customers or flag purchases using disposable emails.

Key Takeaways:

- Why Custom Rules Matter: Generic systems often miss specific risks unique to your business. Custom rules help you better manage fraud while reducing false positives that frustrate legitimate customers.

- Common Risk Indicators: Track patterns like mismatched billing and shipping addresses, disposable emails, high transaction amounts, or velocity indicators (e.g., multiple charges from the same IP).

- Steps to Build Rules:

- Analyze historical fraud data to identify patterns.

- Use attributes like transaction details, geography, and customer history to set conditions.

- Combine multiple conditions to reduce false positives.

- Testing and Deployment: Use sandbox testing and backtesting with historical data to ensure rules are effective. Start with "Review" actions before moving to "Block" for high-risk cases.

- Continuous Monitoring: Regularly review and update your rules to keep up with evolving fraud tactics and business needs.

Custom fraud rules give you control over how aggressively you handle suspicious transactions, helping protect revenue while maintaining a smooth customer experience.

How to Identify Fraud Patterns and Risk Indicators

Common Fraud Risk Indicators and Recommended Actions

To create effective fraud prevention strategies, you first need to understand how fraud manifests in your business. This involves analyzing transaction history, pinpointing critical signals, and identifying the types of fraud that threaten your revenue the most.

Review Your Historical Fraud Data

Start by examining past fraud cases to uncover patterns you may have missed. Focus on data from the last 30 days, and clearly define fraud indicators such as disputed payments, early warnings, or refunded transactions.

Compare the ratio of fraudulent to legitimate transactions across variables like billing states, card BINs, or risk scores. For example, you might find that certain regions have a higher rate of fraud compared to legitimate payments. Use filters to detect overlapping risk factors, such as a mismatched billing and shipping state combined with a high transaction amount. These combinations can often reveal hidden vulnerabilities.

Look for trends like accounts making purchases immediately after signup, clusters of fraud within specific card networks or countries, or high-frequency activity from a single IP or email address. Pay close attention to repeated attempts from the same IP, card number, or email, as these may indicate card testing or "cashing" schemes. Before implementing any new fraud rule, test it against at least six months of historical data to measure its impact on legitimate transactions, fraudulent activity, and blocked payments.

This type of analysis helps prioritize the risk indicators that matter most to your business.

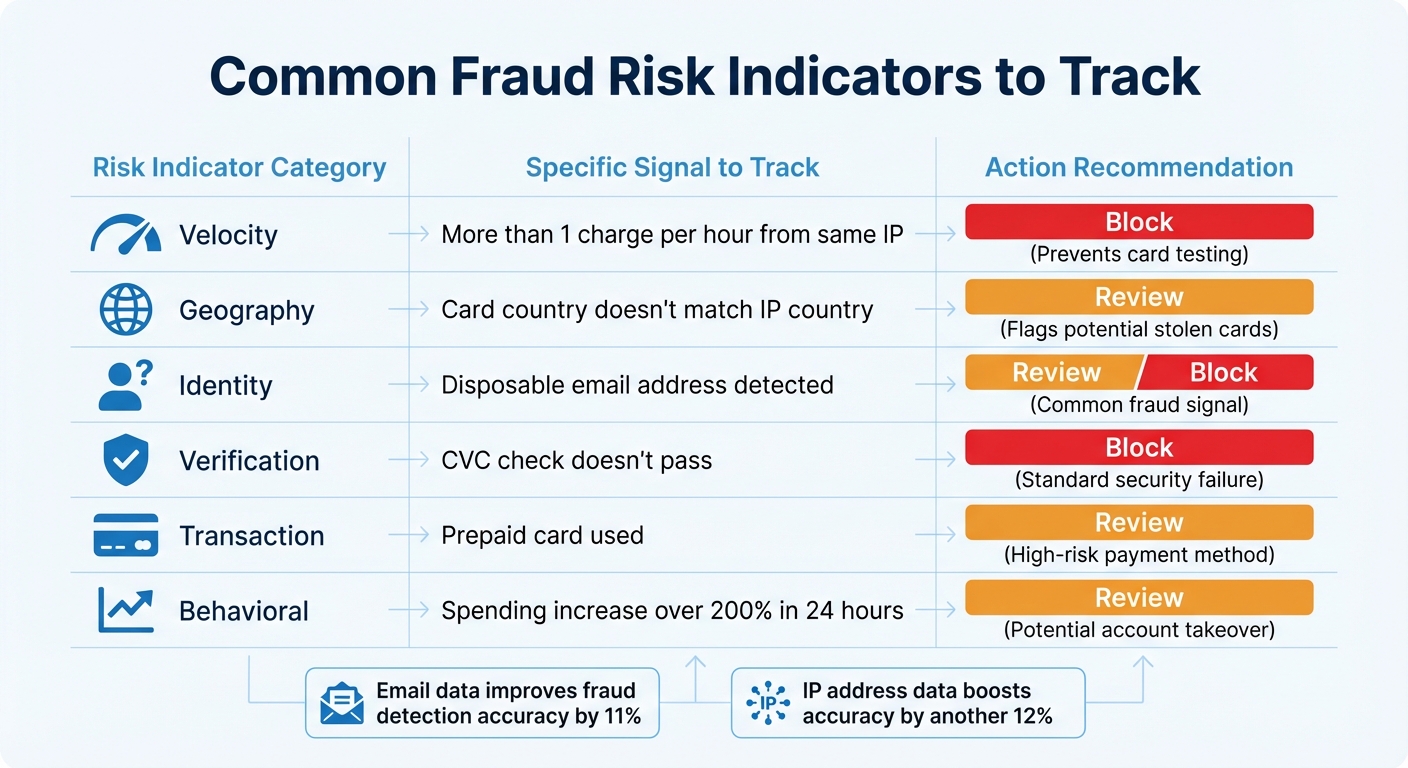

Common Risk Indicators to Track

Certain fraud signals are common across industries and should be prioritized when creating fraud prevention rules. For instance, disposable emails and phone numbers are frequently used by fraudsters and are key identity signals to monitor. Including email address data in fraud detection models can improve accuracy by 11%, while adding IP address data boosts accuracy by another 12%.

Geographic mismatches - such as differences between the card-issuing country, the user’s IP location, and the shipping or billing addresses - are strong red flags for stolen cards. Velocity indicators are another important factor; they detect automated attacks by tracking how often certain actions occur, like multiple successful authorizations from the same IP within an hour. Similarly, failures in CVC or AVS checks should prompt immediate review or blocking, as legitimate customers typically pass these standard security checks.

Transaction anomalies are also worth monitoring. Watch for unusually high amounts on first-time purchases, sharp spending increases (e.g., more than 200% in 24 hours), or the use of prepaid cards. Additionally, some product categories, such as electronics, baby formula, and personal hygiene items, are frequently targeted by fraudsters due to their high resale value.

| Risk Indicator Category | Specific Signal to Track | Action Recommendation |

|---|---|---|

| Velocity | More than 1 charge per hour from same IP | Block (Prevents card testing) |

| Geography | Card country doesn’t match IP country | Review (Flags potential stolen cards) |

| Identity | Disposable email address detected | Review/Block (Common fraud signal) |

| Verification | CVC check doesn’t pass | Block (Standard security failure) |

| Transaction | Prepaid card used | Review (High-risk payment method) |

| Behavioral | Spending increase over 200% in 24 hours | Review (Potential account takeover) |

By identifying these patterns, you can better understand which fraud risks are most relevant to your business.

Assess Your Business's Fraud Risks

Once you've analyzed your data and identified key risk indicators, assess how different types of fraud impact your business. Not all fraud poses the same level of threat. Categorize risks based on their nature to focus your efforts: Payment Abuse (fraudulent transactions), Promo Abuse (exploitation of referrals or discounts), Content Abuse (spam or harmful posts), and Account Abuse (fake signups or account takeovers). Different business models will face unique challenges.

Leverage AI-generated risk scores - labeled as "highest", "elevated", or "normal" - to prioritize transactions that may require manual review. Start with monitoring rules that allow you to track patterns without immediately disrupting legitimate sales. Tailor your rules further by incorporating custom metadata, such as product SKUs, shipping speeds, or customer loyalty status, to address your business's specific needs.

How to Build Custom Fraud Prevention Rules

Turning identified fraud patterns into actionable rules is the key to effective fraud prevention. A simple rule structure works best: {action} if {attribute} {operator} {value}. For example, you could use, "Block if :amount_in_usd: > 1000" or "Review if :card_country: != :ip_country:". This format keeps things clear and makes it easier to align rules with the specific risks you've identified.

Set Your Rule Parameters

Start by selecting the key attributes that will define your rule conditions. These attributes can come from a variety of data categories, such as:

- Transaction details: Includes elements like payment amount, currency, and method.

- Device signals: Covers factors like IP address, device fingerprinting, or anonymous IP detection.

- Customer history: Looks at metrics like email account age or past disputes.

For instance, you could block transactions where the card country doesn't match the IP country, especially if the AI risk score indicates a higher level of risk.

Velocity rules are particularly useful for identifying automated fraud attempts. These rules track how often specific actions occur within a given time frame - hourly, daily, or weekly. A common example is blocking a card if it’s used for more than five declined charges within 24 hours, a pattern often linked to card testing. For reference, hourly velocity buckets cover 3,900 seconds, while daily ones span 90,000 seconds.

You can also incorporate post-authorization checks into your rules. These include CVC verification and Address Verification Service (AVS) results, which come from the card issuer and provide extra assurance of card ownership. Adding custom metadata - like product categories, shipping speeds, or customer loyalty levels - can help create highly specific rules that might catch fraud scenarios standard tools miss.

To keep rule management simple, use lists instead of creating individual rules for every scenario. For example, instead of writing separate rules for each high-risk country, create a single list called @blocked_countries and reference it in one rule: Block if :card_country: in @blocked_countries. Functions like is_missing can also help manage cases where certain data points are unavailable, ensuring your rules stay consistent.

| Attribute Category | Examples | Use Case |

|---|---|---|

| Transaction | :amount_in_usd:, :currency:, :payment_method_type: |

Setting limits on high-value orders |

| Location | :card_country:, :ip_country:, :ip_state: |

Detecting geographic mismatches |

| Device/Tech | :device_fingerprint:, :is_anonymous_ip: |

Identifying bot activity or masked identities |

| Velocity | :total_charges_per_email_hourly:, :declined_charges_per_card_daily: |

Preventing card testing attacks |

| Post-Auth | :cvc_check:, :address_zip_check: |

Verifying card ownership with issuer |

Once the parameters are in place, refine your rules to reduce the risk of misclassifications.

Reduce False Positives

Broad rules can end up blocking legitimate transactions, so it’s better to combine multiple conditions to pinpoint fraud more accurately. For example, instead of blocking all prepaid cards, only block them when paired with a disposable email address. Similarly, flag high-value transactions only when the AI risk score is "elevated" or "highest".

Machine learning risk scores can further improve rule precision. Before deploying a new rule, backtest it against six months of historical data. This testing phase helps you evaluate whether the rule is too strict or too lenient.

If you're unsure about a rule's impact, set its action to "Review" as a precaution.

Choose the Right Action: Block, Review, or Allow

Once your rules are fine-tuned, the next step is deciding the appropriate action for each one. Every rule must specify an action, and the choice depends on your confidence level and the transaction's risk profile. Actions are processed in a specific order: Request 3D Secure (3DS) > Allow > Block > Review.

- Block transactions when there's high confidence in fraud detection. Examples include failed CVC or AVS checks, exceeding velocity limits, or when multiple high-risk signals align.

- Use Review for suspicious activity that needs human evaluation, such as geographic mismatches. This action lets the transaction proceed but flags it for manual inspection, giving you a chance to gather more information without outright rejecting a potentially legitimate sale.

- Allow rules should be used sparingly, as they override all other risk assessments. These are best reserved for scenarios like transactions from VIP customers, verified call center orders, or whitelisted IP addresses.

- For high-risk transactions, you can use Request 3DS to prompt additional authentication, shifting liability to the card issuer. Ensure your 3DS and Block rules work together so that unsupported or failed 3DS attempts result in appropriate restrictions.

| Action Type | When to Use | Impact on Transaction |

|---|---|---|

| Request 3DS | High-risk transactions requiring cardholder verification | Prompts additional authentication; shifts liability to issuer |

| Allow | Trusted IPs, VIP customers, verified call center orders | Processes normally; overrides Block/Review rules |

| Block | High-confidence fraud signals or restricted payment methods | Rejects payment immediately |

| Review | Suspicious patterns requiring human judgment | Processes payment but flags for manual inspection |

Testing and Deploying Your Custom Rules

To ensure your custom fraud rules are effective without disrupting legitimate transactions, thorough testing and careful deployment are key. Before rolling out any rules, you need to confirm they won't inadvertently block real customers or fail to catch fraudulent activities. A step-by-step approach is the safest way to achieve this balance.

Test Rules in a Sandbox Environment

Start with shadow testing, which runs your new rules alongside your live setup without affecting actual transactions. This allows you to observe how the rules behave in real-time traffic and identify any issues before they impact customers.

You can also use backtesting, where historical data - typically from the past six months - is used to simulate how the rule would have performed. This helps you estimate false positives and measure the fraud detection rate.

In the early stages, set your rules to count mode. This mode logs matches without altering transaction paths or blocking users, giving you a clear view of how the rules perform without disrupting operations. For instance, AWS WAF provides test credentials (email: [email protected], password: WAF_TEST_CREDENTIAL_PASSWORD) to confirm that your system correctly flags compromised credentials. To test volumetric rules, try creating at least five accounts from the same session within 30 minutes to verify they trigger as expected.

When introducing new rules, assign them lower priority (higher numerical rank in some systems). This ensures your proven rules continue to handle known threats first. Also, set the initial rule action to "Review" rather than "Block." This allows flagged transactions to proceed while being marked for manual review.

After testing, move on to measuring the rule’s performance to ensure it meets your goals.

Measure Rule Performance

Tracking key metrics is essential to evaluate how well your rules are working. Metrics like the fraud block rate indicate how effectively your rules stop fraudulent payments, while the false positive rate shows how often legitimate transactions are mistakenly flagged. Keep an eye on the number of transactions sent for manual review - too many can overwhelm your team.

Compare the results of your test strategy with your live strategy to assess changes in fraud prevention. Also, monitor the conversion impact to ensure that additional verification steps don’t negatively affect customer experience or payment completion rates. Other metrics, like dispute and refund rates, can help you identify fraud that slips through. Watch for unexpected spikes or drops in rule triggers to spot potential issues.

| Metric | Purpose | What to Watch For |

|---|---|---|

| Fraud Block Rate | Measures how well fraud is detected | Should increase with better rules |

| False Positive Rate | Tracks impact on legitimate users | Should decrease over time |

| Review Rate | Measures operational workload | Keep manageable to avoid bottlenecks |

| Dispute Rate | Tracks fraud that bypasses rules | Should trend downward |

"A good block rule results in significantly more fraudulent payments blocked than legitimate payments." - Stripe

Once you've confirmed the rules are effective, the next step is a controlled production deployment.

Deploy Rules to Production

When testing shows your rules are ready, follow a structured process for deploying them. Begin with offline backtesting in your data warehouse to establish a baseline, then move to online backtesting to confirm the rule syntax works in your fraud engine. Require a dual review of the rules before rolling them out.

Keep new rules in shadow mode for at least a week to monitor their live performance and ensure they align with your historical predictions. During this time, manually review 50 to 100 flagged cases to verify accuracy. Introduce high-threshold safety rules to catch extreme fraud spikes as an added precaution.

"The safest way to ship fraud rules is to treat release as a process, not an event." - Chen Zamir, Head of Fraud Strategy, Sardine

Fraud tactics evolve over time, so even the best rules will lose effectiveness eventually. Plan to review and update your rules every six to 12 months to stay ahead of fraudsters and avoid "rule rot".

Monitoring and Improving Your Fraud Rules

Once you've deployed your custom fraud rules, the work doesn't stop there. Continuous monitoring and fine-tuning are essential to keep up with shifting fraud tactics. Fraudsters change their methods over time, so rules that work today might not be effective tomorrow. Worse, outdated rules could start blocking legitimate customers as your business evolves. Regular updates ensure your fraud prevention stays sharp without causing unnecessary disruptions.

Review Rules Regularly

It's important to regularly evaluate how your rules are performing. Keep an eye on performance charts for any unusual spikes or drops in rule matches. These can be signs that fraudsters have adjusted their strategies or that a rule has become too broad. If you notice that a rule is flagging too many legitimate transactions, refine it by adding more specific conditions. For instance, instead of blocking all prepaid cards, you could narrow it down to prepaid cards used with disposable email addresses.

Fraud risk management typically follows four key steps: Detection, Investigation, Confirmation, and Refinement. This structured approach helps you stay proactive, identifying new fraud patterns and addressing them before they cause major issues.

"Assessing fraud risk is a continuous process of identifying attack vectors, patterns, and scenarios and mitigating them." - Stripe

Use Threat Intelligence

External threat intelligence can help you spot risks that haven't yet appeared in your own data. Incorporating tools like IP blacklists, disposable email provider databases, or Early Fraud Warnings from card issuers can give you a head start in recognizing fraud patterns. These external signals can highlight risky behaviors - such as transactions linked to certain card brands, IP addresses, or geographic regions - that your internal systems might overlook.

Modern fraud systems often include AI-powered tools that simplify rule creation. These tools allow you to translate plain-English instructions into complex rule syntax. For example, if you notice a sudden rise in chargebacks from a specific region, you could quickly create a rule like, "Block transactions over $500 from IP addresses in [region] using prepaid cards", without needing coding expertise. Integrating this kind of intelligence into your workflow can make your fraud prevention efforts more agile and precise.

Document Rules and Maintain Compliance

Clear documentation of your fraud rules is a must. Record each rule's logic, purpose, and performance history to create an audit trail. This is essential for meeting regulatory requirements and maintaining internal accountability. Categorize your rules - such as labeling them as "Legal", "Fraud", or "Business" - to make it easier to differentiate between compliance-focused rules and those aimed at fraud prevention. Proper documentation also helps your team understand the reasoning behind each rule, making updates or retirements smoother as your business needs change.

Conclusion

To create effective fraud prevention rules, start by analyzing historical data, setting clear parameters, and testing your rules against past transactions. This approach helps strike a balance between security and user experience. Well-crafted rules can lead to impressive results, such as reducing fraudulent registrations by 90% and cutting manual review time by 80%. Keep in mind, however, that the success of these rules hinges on regular evaluation and updates.

Fraud prevention is not a "set it and forget it" process. Fraudsters adapt quickly, so your system must evolve too. Regular monitoring, refinement, and thorough documentation are critical for maintaining effective rules and staying compliant with regulations like the Red Flags Rule and the Sarbanes-Oxley Act (SOX). Use performance metrics to identify when adjustments are needed, and don’t hesitate to retire rules that no longer serve their purpose.

If you're uncertain about blocking transactions outright, start with review actions instead. This method allows you to collect valuable data on potential false positives without risking legitimate sales. Over time, as you gain confidence in your rule set, you can move toward more decisive measures - like blocking high-risk transactions or using 3D Secure authentication for an added layer of verification.

FAQs

How do custom fraud prevention rules help minimize false positives?

Custom fraud prevention rules let you set up criteria that align with your business's unique needs. For example, you can focus on monitoring specific IP addresses, transaction amounts, or patterns in user behavior. By honing in on these precise signals, the system can better differentiate between legitimate activities and possible fraud.

This approach helps cut down on mistakenly flagging valid transactions as suspicious, reducing false positives. The outcome? A more seamless experience for your legitimate customers while keeping fraud detection sharp and effective.

What are the most important risk factors to consider when creating fraud prevention rules?

When setting up custom fraud prevention rules, it's essential to focus on signals that can clearly differentiate between genuine activity and potential fraud. Start with IP reputation and geolocation - look out for blacklisted IP addresses or those originating from high-risk regions. Another key area is device and browser fingerprints, which can reveal mismatched or suspicious configurations. Keep an eye on transaction anomalies, such as unusually large purchases or sudden spikes in spending patterns. Additionally, velocity patterns - how quickly users perform actions like logins or payments - can be a strong indicator of fraudulent behavior.

Other red flags to monitor include payment method inconsistencies, such as mismatched card types or issuing banks, as well as billing and payment location discrepancies. Pay attention to email or account creation signals, like the use of disposable email addresses or recently created accounts initiating high-value transactions. By concentrating on these primary indicators, you'll be better equipped to catch common fraud tactics while allowing room for tailored checks specific to your business's unique risks.

What’s the best way to test and implement custom fraud prevention rules?

To test and deploy fraud prevention rules effectively, start by defining the rule's logic based on specific fraud patterns. For example, you might focus on unusual transaction amounts or activity from suspicious IP addresses. Always begin testing in a non-production environment like a sandbox or staging area. This ensures live traffic remains unaffected while you validate the rule's accuracy.

Use realistic test data - such as recent transactions or synthetic examples - to confirm the rule identifies fraudulent activity without blocking legitimate users. Keep an eye on metrics like false positives, false negatives, and approval rates to refine the rule further. If your system allows, activate the rule in monitoring mode to observe its behavior on live traffic without enforcement.

When you're confident in the rule's performance, roll it out gradually, starting with a small segment of live traffic. This phased approach helps you catch any unexpected issues before full deployment. Finally, keep reviewing and tweaking the rule regularly, as fraud tactics can change over time. This ongoing adjustment ensures the rule stays effective while minimizing disruptions for genuine users.